If you invest in stocks, bonds, stock indices, real estate, debt instruments, or cryptocurrency and decide to sell, one thing remains constant for all of us: you must pay capital gains tax. Even if you invest in assets that are supposedly untraceable, the duty falls on you to self-report the gains, and people have been convicted for failing to do so. Latvia’s capital gains tax (CGT) was 20% until it was raised to 25.5%, with even higher rates for larger gains. Should this decision have been made, and what will be the consequences?

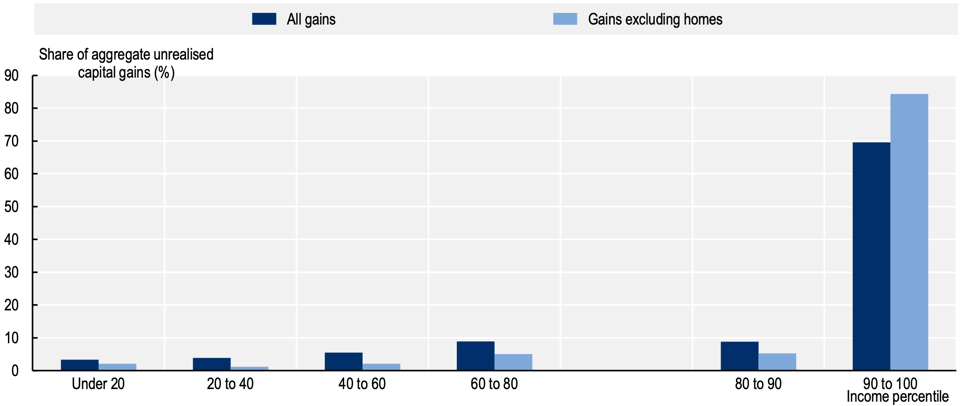

The first – and probably most convincing – argument is the fact that CGT is a very progressive tax. In the graph, the percentage of aggregate unrealised capital gains is plotted against income percentiles in the United States. It is very clear that the wealthy would have the most to lose from an increase in CGT. This means that increasing CGT is a relatively popular and easy way to raise short-term tax revenue without significantly affecting the average consumer. For example, an increase in value-added tax (VAT) would be far more painful for ordinary people.

However, this analysis is quite simplistic – what about the long-term effects? Interestingly, increases in CGT often have relatively little impact on the short-term price of assets. This is due to the “lock-in” effect – since selling the asset now has a lower immediate benefit, people may choose to hold onto their assets in the hope that CGT will be reduced in the future. In some cases, this can even lead to a short-term price increase.

On the other hand, we must also consider the effect on new investment. While Latvia would be ranked 12th in the EU with the new tax rates, it does not enjoy the same advantages as Scandinavian countries or France. Therefore, the most relevant comparison would be with the other Baltic States. Lithuania has a 15% CGT rate for amounts not exceeding 250,000 EUR, rising to 20% above that threshold, while Estonia maintains a flat 20% rate. Latvia is already the least attractive investment destination among the Baltics – in Q4 of 2024, total foreign investment was by far the lowest among the three, especially when calculated per capita. An increase in CGT only worsens Latvia’s competitiveness at a time when a boost in foreign investment is desperately needed.

A higher CGT could also encourage tax arbitrage schemes, where investors declare profits in more favourable tax regimes. Although this may not pose a significant threat due to Latvia’s relatively small securities market, where most investment comes in the form of capital that is harder to disguise, smaller investors may still choose to hold their assets in foreign wallets. In such cases, the Latvian tax authorities are effectively powerless, and these investors could launder the money back into Latvia without detection. Over time, this undermines both the effectiveness of the tax policy and trust in its fairness. Moreover, it sends the wrong message to small domestic investors who might otherwise be willing to report their earnings honestly and participate in the local market.

In summary, it was argued that the increase in CGT in Latvia was a poor decision in the long term. While there may be short-term benefits, the country will undoubtedly be worse off in the long term, becoming less competitive within the Baltic region and lacking many of the unique features that attract foreign capital. Hopefully, Latvia’s government will recognise this and reconsider the decision.

– Rudis Freipics