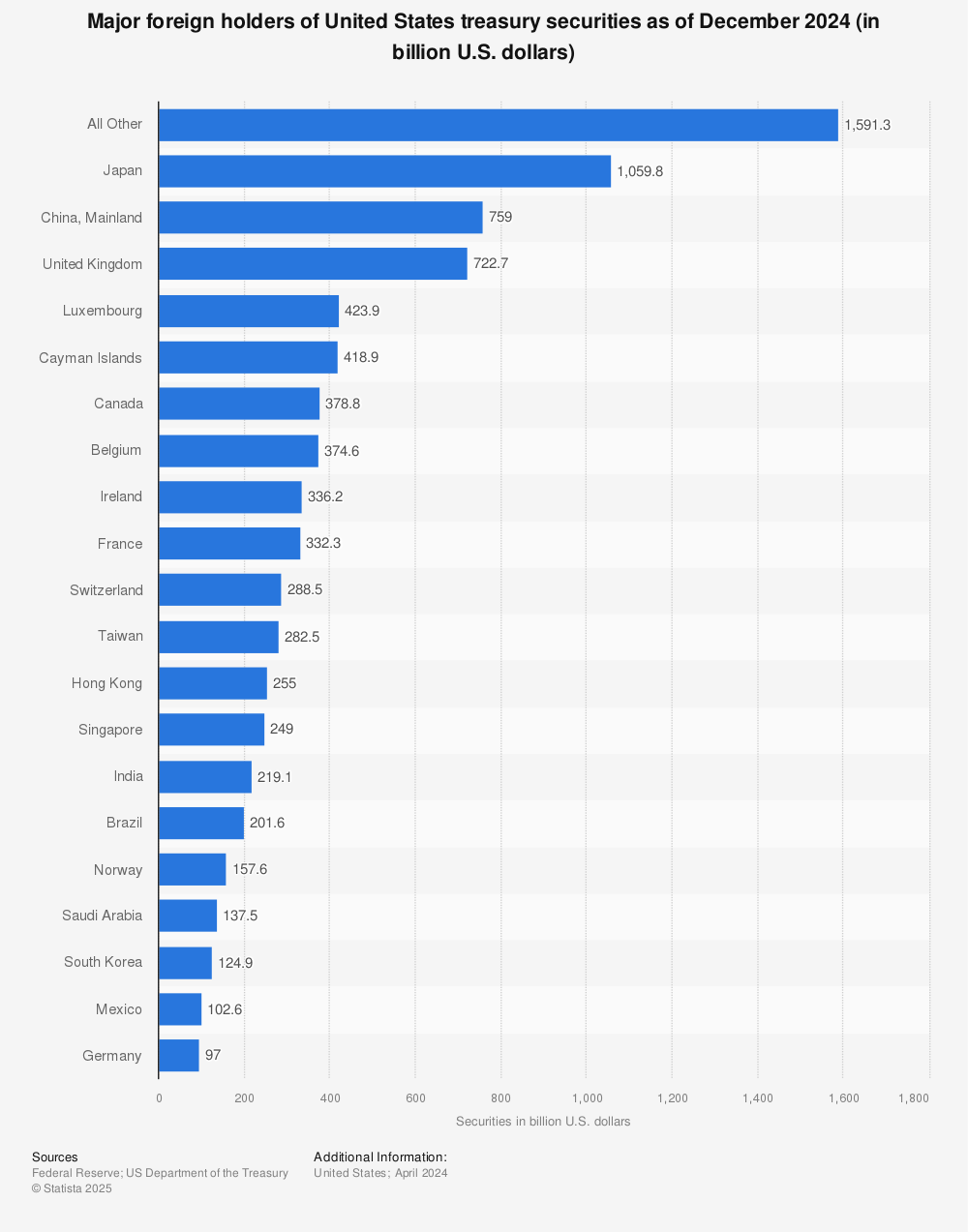

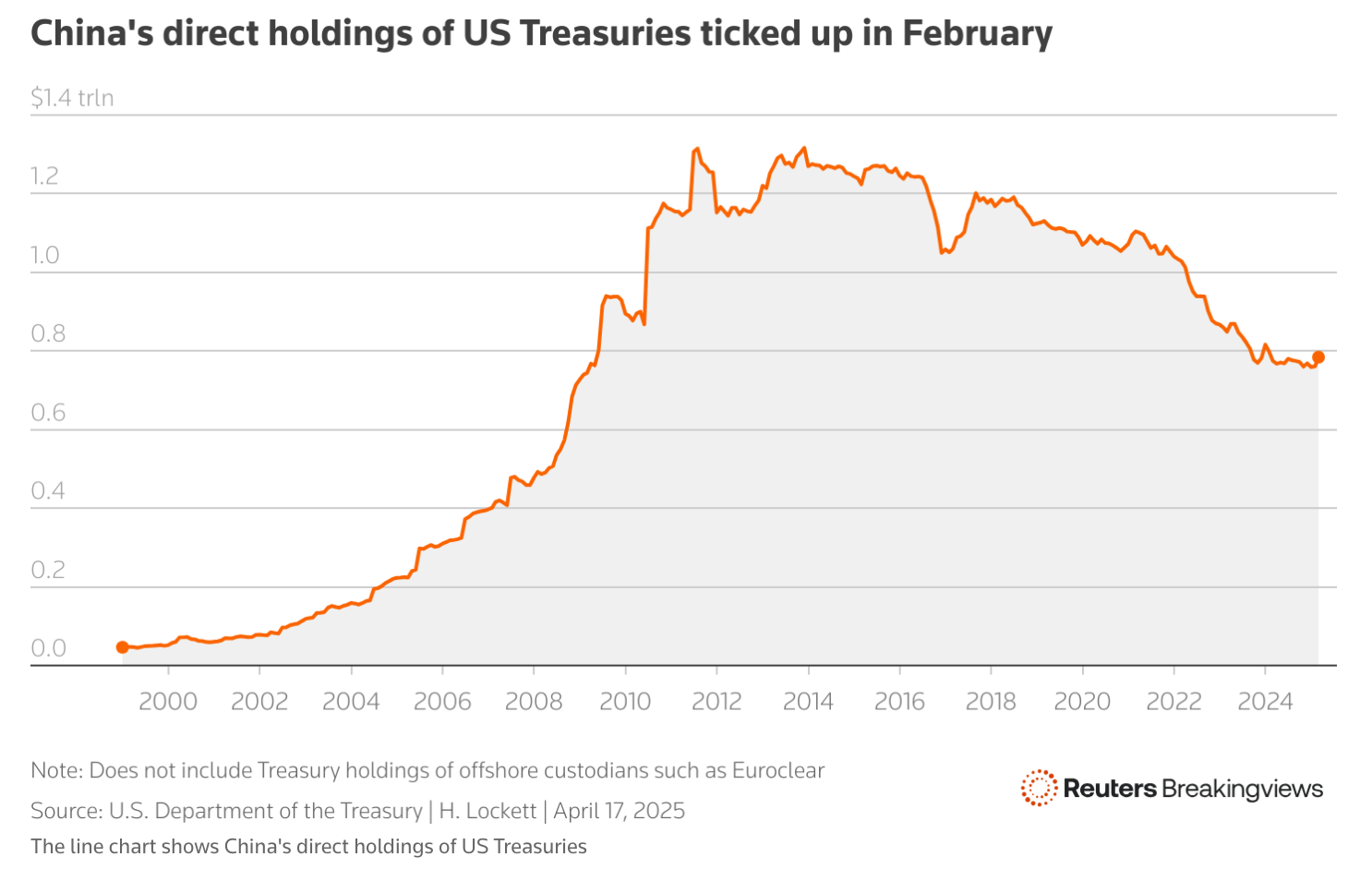

As tensions between China and the U.S. keep rising, one of China’s more quiet but potentially powerful tools could prove to be its stake in the U.S. government debt. Alongside Japan, China has long been one of the largest foreign holders of U.S. Treasuries, peaking at over $1.3 trillion in 2013. But that number has been falling, and as of February 2025, it is below $800 billion. This change is pointing more towards a strategic shift away from the US rather than just reserve management.

China isn’t dumping Treasuries overnight, but it is repositioning. It’s been steadily building up gold reserves and moving into non-dollar assets, particularly euro-denominated ones like German bunds. This change can also be somewhat seen in the recent market reaction, more specifically, the U.S. 10-year yields are up, and the German bund yields are down, as well as the appreciation of the euro. All signs point to capital being moved from the U.S. to the EU. This doesn’t mean China is liquidating their whole standing, but the idea of reducing its exposure to the U.S. is getting clearer.

All of this is happening while U.S.–China tensions are high. Export controls, tech restrictions, and tariffs are affecting both sides, especially during the more recent escalations in the trade war. In that context, the idea of China weaponizing its Treasury holdings, whether as leverage or as financial retaliation, doesn’t sound that far anymore.

But it’s not exactly a risk-free move. A sudden sell-off would push down the price of Treasuries and raise yields, which would hurt the value of China’s remaining holdings. It would also flood China with U.S. dollars, which they’d then have to convert, appreciating the yuan. That’s not what China would want; with weak demand and pressure on exports, it should try to boost domestic growth and keep the yuan competitive. Although they could instead, as discussed before, convert their holdings into euro bonds or just hold the dollars to avoid this from happening.

For the U.S., this action could also bring consequences. If foreign demand for Treasuries keeps dropping, it could push up long-term borrowing costs over time, especially with the U.S. running big deficits. Although Japan and domestic buyers still hold the majority, without China, the market becomes more sensitive and potentially more volatile during times of stress. That could mean steeper yield curves and shakier market conditions going forward.

This idea of weaponizing financial assets also adds a whole new layer of uncertainty. This could change how long-duration bonds and dollar-based assets are priced, and shift more attention toward geopolitical risks. For investors, the implications are wide-ranging. Higher yields make short-duration bonds more attractive relative to long-duration ones. Demand for gold and other real assets could rise as investors look for investments outside of traditional currency or fixed-income markets. Additionally, the

Moreover, the undertones of China’s repositioning could drive increased demand for non-traditional markets like gold and other real assets.

Having said that, the U.S. Treasuries are still among the safest and most liquid assets in the world. The U.S. dollar remains dominant, and any shift away is rather unlikely and will take time. But China’s gradual retreat signals a deeper rethink of capital allocation through a more political approach. This is less about panic and more about positioning in the world of global finance driven by market logic, politics, and power, especially if the tensions continue.

Overall, these developments demand attention as the slow, deliberate nature of China’s actions does not diminish their potential impact. As global debt levels rise and the global competition intensifies, the balance of financial power could perhaps begin to see a shift.

– Marcus Paas